Private Credit AI Risk: The BIS Found $115 Billion in Software Loans Priced As If AI Did Not Exist

The BIS found business development companies hold $115 billion in software loans and charge no extra spread for AI disruption risk. Here is what that means.

The Bright Recap

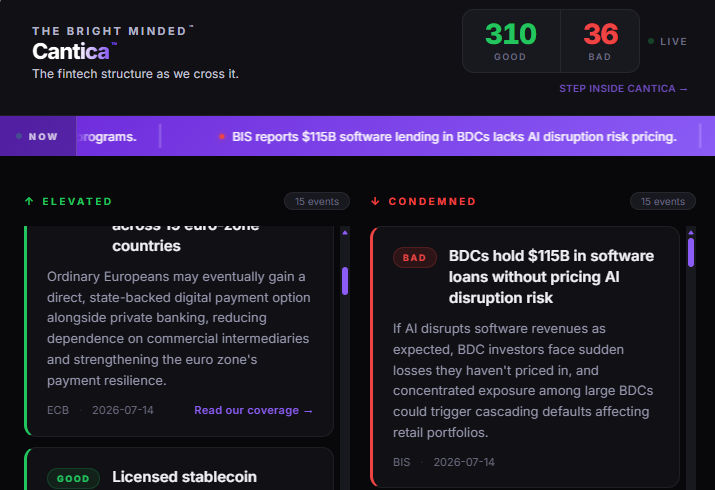

The Bank for International Settlements published Bulletin 128 on 14 July 2026. It finds that business development companies, a regulated form of private credit lender in the United States, have lent around $115 billion to software firms, roughly a fifth of all their lending and over 80% of their technology portfolios.

Software borrowers pay broadly the same spreads as everyone else, and no discount is applied to lenders concentrated in the sector. Fewer than 1% of these loans are behind on payments. Spreads have narrowed, five lenders hold about 37% of the exposure, and around 60% of software lending goes to firms that borrow from seven or more of these lenders at once.

To know more about this topic, read our related articles:

- What the BIS flagged last month

- How lending markets actually operate

- The hidden cost problem in AI

- Who is deploying AI into portfolios

- Financial technology explained

Bright Answers

What is a business development company?

A regulated US lender that provides credit to small and mid-sized firms. There were around 170 of them at the end of 2025, holding roughly $550 billion in assets, and they must report their holdings loan by loan to the Securities and Exchange Commission every quarter, which makes them the visible portion of an otherwise opaque private credit market.

Are these software loans in trouble?

Not on any current measure. Fewer than 1% are behind on payments, a better rate than the rest of these portfolios. The BIS point is that backward-looking credit metrics would not yet show a revenue shock, and that spreads have narrowed rather than widened while the underlying risk grew.

Private credit AI risk has one specific shape, and the Bank for International Settlements (BIS) has now measured it. Lenders known as business development companies (BDC) have put around $115 billion into loans to software firms, roughly a fifth of everything they lend and more than 80% of their technology books, and they charge those borrowers no more than they charge anybody else. Bulletin 128, published on 14 July 2026 by Fernando Avalos, Giulio Cornelli and Egemen Eren, sets out the numbers. The interesting part sits in what a credit market is structurally able to see.

A loan is priced against the probability that cash arrives on schedule. Generative artificial intelligence (AI) does not miss a payment. It removes a subscription from a mid-market software vendor long before that vendor's cash position tightens enough to trouble a covenant, and for the whole of that interval the loan looks like a loan that is fine.

Meet Cantica, the Fin-Tech intelligence layer behind The Bright Minded.

Cantica's Purgatorio called this bad, and I would put it differently

Cantica's Purgatorio marked the finding as bad, and the exposure reading is right.

On the other hand, the BIS authors offer two interpretations and decline to choose. The reassuring one holds that these lenders apply a consistent risk standard whatever the sector, and lend to software firms only where the fundamentals match their other borrowers, in which case identical spreads are correct.

The uncomfortable one holds that a long private credit boom loosened underwriting through competition for deals, in which case the risk is underpriced and any shock produces losses that arrive together.

Software became the safest thing in private credit, and then it stopped being safe

Direct lenders spent a decade moving into technology for reasons that were sound at the time. Software firms delivered recurring subscription revenue, high margins and minimal capital needs, which is close to the ideal borrower profile for anyone with a fixed coupon to collect. Lending to information technology climbed to nearly $140 billion, about a quarter of all BDC loans and their second-largest sector after business services. Almost all of that growth was software.

The BIS notes that around three quarters of the software exposure sits in horizontal and workflow products, meaning productivity, application and automation tools. Those are the categories where an AI system substitutes most directly for the thing the customer was paying for. The borrowers most exposed to AI substitution are the borrowers this money went to, and the hidden cost problem inside AI economics has a mirror image on the lending side that has drawn far less attention. Software firms that are still growing while cutting staff are the visible edge of the same margin pressure.

Equity markets have already made the call that credit markets have not

Public equity investors reached a verdict some time ago. Software stocks carried a valuation premium over the wider technology sector at the end of 2021. From December 2022, after ChatGPT reached the public, that premium narrowed and had turned into a discount by the end of 2025.

Credit did not follow. Spreads on software loans converged with spreads on everything else, and the compression was steepest on newly issued loans and on loans from non-listed BDCs, the segment facing the least market scrutiny. The listed lenders themselves trade at similar price-to-dividend ratios whether they are heavy in software or light in it. Two markets are looking at the same borrowers and disagreeing, and only one of them can update daily.

Equity prices reset every time a shareholder changes their mind, while a loan written at a fixed spread holds that price until the borrower stops paying, so the disagreement gets resolved by credit moving towards equity or by equity being proved wrong, and nothing in the loan book can tell you which before the fact.

Why the numbers look excellent and prove very little

Fewer than 1% of software loans are behind on payments, a better rate than the rest of these portfolios. The BIS treats that figure with the caution it deserves. Lost revenue works its way through a company slowly before it ever shows up as an unpaid instalment, and payment-in-kind arrangements let a borrower settle interest by issuing more debt instead of handing over cash, which pushes the moment of visibility further out again.

Anyone who has followed how lending markets actually operate will recognise the pattern, and readers who followed the BIS on settlement infrastructure last month will recognise the institution's habit of publishing the number nobody else wanted to compute. The instruments in use here are excellent at recording what has already gone wrong. They contain no field for a risk that currently exists only as a competitive dynamic.

The plumbing that turns a repricing into an event

Three structural features determine what happens if software credit does weaken. Around 60% of software lending now goes to firms borrowing from seven or more BDCs, up from under 10% in 2015, so a sector-wide shock would land on many balance sheets in the same quarter. The five largest lenders hold about 37% of all software loans and the ten largest hold more than half, which concentrates the losses. Roughly a quarter of the exposure sits in non-traded vehicles where investors exit by redeeming shares, usually capped at 5% of assets under management per quarter, and one large non-traded BDC went past its cap for the first time in early 2026.

The BIS also lists the protections, and they are substantial. Statutory limits keep leverage well below bank levels, most of the lending is senior and secured with terms that allow a lender to step in at the first sign of trouble, and listed BDCs run on equity that investors have no right to pull. These defences are the reason this is a story about pricing rather than a story about collapse.

What a professional outside this market should take from it

The transferable lesson has nothing to do with software or with private credit. Every risk model in financial technology and in traditional finance is trained on the shape of past failures, and AI disruption has no past shape yet. It shows up as a competitor able to build the same product at a fraction of the cost, and it enters a lender's system only once that competitor has taken enough revenue to break a payment schedule.

The same blindness sits inside the firms deploying AI into their portfolios, inside every corporate credit assessment being written this quarter, and inside the assumptions a professional makes about how durable their own employer's revenue is. The BIS has found the one corner of the market where somebody is legally obliged to publish the exposure loan by loan.

A credit market can only charge for danger it has already been shown, which is why the loans that look safest today are the ones underwritten against a competitor nobody has met yet.

Editor's note

Every piece published on The Bright Minded goes through careful verification, but mistakes can happen. If you spot an error, have additional information, or want to flag anything, write to rosalia@thebrightminded.com.