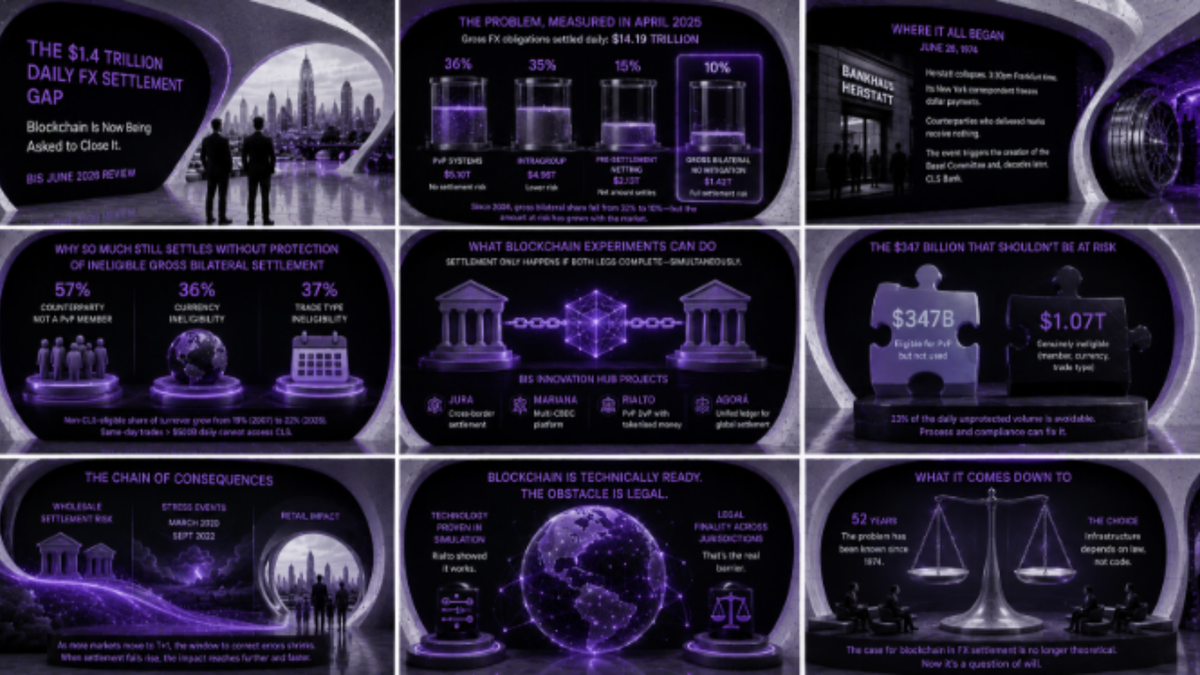

BIS June 2026 Review: The $1.4 Trillion Daily FX Settlement Gap That Blockchain Is Now Being Asked to Close

The BIS June 2026 Quarterly Review found $1.4 trillion in FX trades settle daily with no risk protection, down from 32% in 2006 to 10% — and blockchain is the next candidate.

FX settlement risk — the danger that one party in a currency trade delivers and receives nothing because the counterparty defaults first — has been documented, measured, and institutionally managed since 1974. The BIS June 2026 Quarterly Review, published today, found it is still happening at $1.42 trillion per day. That is the volume of foreign exchange obligations settling every day on a gross bilateral basis, with no payment-versus-payment system, no netting, and no simultaneous exchange protecting either side.

The same report names distributed ledger technology as the most credible live experimental candidate to close that gap, through four active BIS Innovation Hub projects whose logic reduces to a single principle: a smart contract that will not execute unless both currency legs complete at the same time.

The problem's origin is the following. On June 26, 1974, German regulators shut Bankhaus Herstatt at 3:30pm Frankfurt time. Herstatt's New York correspondent bank immediately froze all outgoing dollar payments. Counterparties who had already delivered Deutsche marks to settle their FX trades received nothing. The collapse triggered the creation of the Basel Committee on Banking Supervision (BCBS) and eventually CLS Bank, which launched CLSSettlement in 2002 as a payment-versus-payment (PvP) mechanism guaranteeing simultaneous exchange for 18 currencies. CLS now processes over $8 trillion daily. It solved a real problem, but left behind what the BIS June 2026 Quarterly Review quantifies for the first time by settlement method rather than by turnover estimates alone.

What the BIS found in April 2025

The 2025 BIS Triennial Survey of FX markets, analysed in the June 2026 review, is the first to classify settlement volumes by the method used. Of the $14.19 trillion in gross obligations settled on an average April day, 36% went through PvP systems and eliminated settlement risk entirely.

A further 35% settled intragroup — between entities within the same banking group — where the risk is lower but not gone. Another 15% went through pre-settlement netting, which reduces gross amounts to a smaller net figure that still requires settlement by other means. The remaining 10%, $1.42 trillion, settled on a gross bilateral basis with no mitigation mechanism in place, exposing each counterparty to the full value of every trade in that pile.

That $1.42 trillion is not a rounding error in a $14 trillion market. It is the portion where a single counterparty failure could produce losses equal to the full principal of every unprotected trade. The BIS notes that settlement fails in April 2025 were tiny — 0.01% of total obligations — but the exposure is not about what happened that month. It is about what happens in the next stress event, when counterparties are failing rather than merely slow. Progress since 2006 is real: the gross bilateral share has fallen from 32% of daily settlement to 10%, driven primarily by greater use of pre-settlement netting rather than by PvP expansion. The absolute amount at risk, however, has grown alongside the market.

Why the fix has not worked

The BIS data reveals three distinct reasons why trades still settle without any protection. The first, accounting for 57% of ineligible gross bilateral settlement, is that the counterparty is not a member of any applicable PvP system. CLS has 76 settlement members and 38,000 third-party participants, which sounds large until you consider that the FX market includes an enormous and growing population of non-bank financial institutions — hedge funds, pension funds, asset managers — whose PvP access is limited or indirect. The share of FX activity handled by non-banks has grown continuously since the BIS began tracking it, and those participants cluster disproportionately in the settlement methods with the least protection.

The second reason, covering 36% of ineligible gross bilateral settlement, is currency ineligibility. CLSSettlement covers 18 currencies. The non-CLS-eligible share of global FX turnover has grown from 19% in 2007 to 22% in 2025. As currencies like the Indian rupee and Chinese yuan take larger roles in global trade, more of the daily settlement volume falls outside the system designed to protect it. The digital dollarization of emerging market economies compounds this: stablecoin transactions in non-major currencies add settlement volume that existing PvP infrastructure was not built to handle.

The third reason, covering 37%, is trade type ineligibility. PvP systems are structured around T+1 and T+2 settlement cycles. Same-day trades — estimated at over $500 billion in daily volume — cannot currently access CLSSettlement because the cutoff times do not accommodate them. As more jurisdictions move securities settlement to T+1 cycles, the demand for same-day FX to fund cross-border securities transactions will grow, and so will the exposure.

What blockchain does that institutions cannot

The BIS Innovation Hub has been running four experiments — Projects Jura, Mariana, Rialto, and Agorá — specifically targeting FX settlement using distributed ledger technology. Project Rialto, completed in December 2025 by the BIS Innovation Hub with the central banks of France, Italy, Malaysia, and Singapore, combined PvP settlement with an automated market maker and tokenised wholesale central bank money in a simulated cross-border payment infrastructure.

The technical report demonstrated that connecting non-tokenised payment systems to tokenised FX and settlement is technically feasible. Project Agorá, the BIS's largest initiative to date, involves seven central banks and 41 private sector participants including JPMorgan, Deutsche Bank, Visa, and Mastercard, building a unified ledger where tokenised assets trade using digital currencies issued by participating central banks.

The reason these experiments matter is structural, not technological. A smart contract on a distributed ledger can be written so that settlement only executes if both payment legs complete simultaneously, the same guarantee CLS provides, but without requiring either party to be a CLS member and without the currency restrictions that leave 22% of global FX turnover outside PvP coverage. The core principle of blockchain — that transactions execute conditionally and verifiably without a central intermediary — is precisely what the access gap in FX settlement requires. The DTCC's move toward blockchain-based securities settlement applies the same conditional logic to a different but adjacent problem.

The gap that institutions admitted

A detail buried in the BIS data deserves attention. Of the $1.42 trillion settling daily without protection, $347 billion was actually eligible for PvP systems. The currency pairs qualified. The counterparties had access. The trade types were covered. They simply did not use PvP settlement, for reasons the BIS describes as operational: missed cutoff times, difficulties managing credit exposure to correspondent banks, and tight payment schedules. Nearly a quarter of the daily unprotected volume is avoidable without any new technology or legal reform.

This is where fintech has a more immediate role than any blockchain experiment. The Global Foreign Exchange Committee (GFXC) updated the FX Global Code in January 2025, introducing an explicit settlement hierarchy and calling on all market participants to review their settlement choices regularly. Getting the $347 billion of avoidable exposure onto PvP requires process and compliance culture, not distributed ledgers.

The harder problem — the $1.07 trillion that is genuinely ineligible due to counterparty membership gaps, currency restrictions, or trade type limitations — is where the experiments matter. And there the obstacle is not whether blockchain can technically replace correspondent banking for FX settlement. Project Rialto demonstrated that it can, at least in simulation. The obstacle is legal: settlement finality across jurisdictions requires enforceable law across borders, not just working code.

What this means beyond the trading floor

The $1.42 trillion figure is a wholesale market number. The counterparties at risk are banks, broker-dealers, and financial institutions. But the chain of consequences runs further. As more jurisdictions adopt T+1 securities settlement cycles, the window to correct FX settlement errors narrows. Settlement fails, currently minimal, could rise. The March 2020 "dash for cash" and the September 2022 UK gilt crisis both showed that stress in wholesale markets reaches retail exposure faster than most observers anticipate.

What the Wall Street resistance to blockchain infrastructure has always revealed is that the problem is not whether the technology works. It is whether the institutions that benefit from the current system have sufficient incentive to replace it. FX settlement risk has persisted for 52 years not because no one understood it, but because the parties best positioned to fix it were also most insulated from the consequences of not fixing it.

The BIS Innovation Hub's four running experiments suggest that position is changing — and that the case for distributed ledger technology in FX settlement is no longer theoretical. Whether it becomes infrastructure depends on law, not code.

Editor's note

Every piece published on The Bright Minded goes through careful verification, but mistakes can happen. If you spot an error, have additional information, or want to flag anything, write to rosalia@thebrightminded.com.