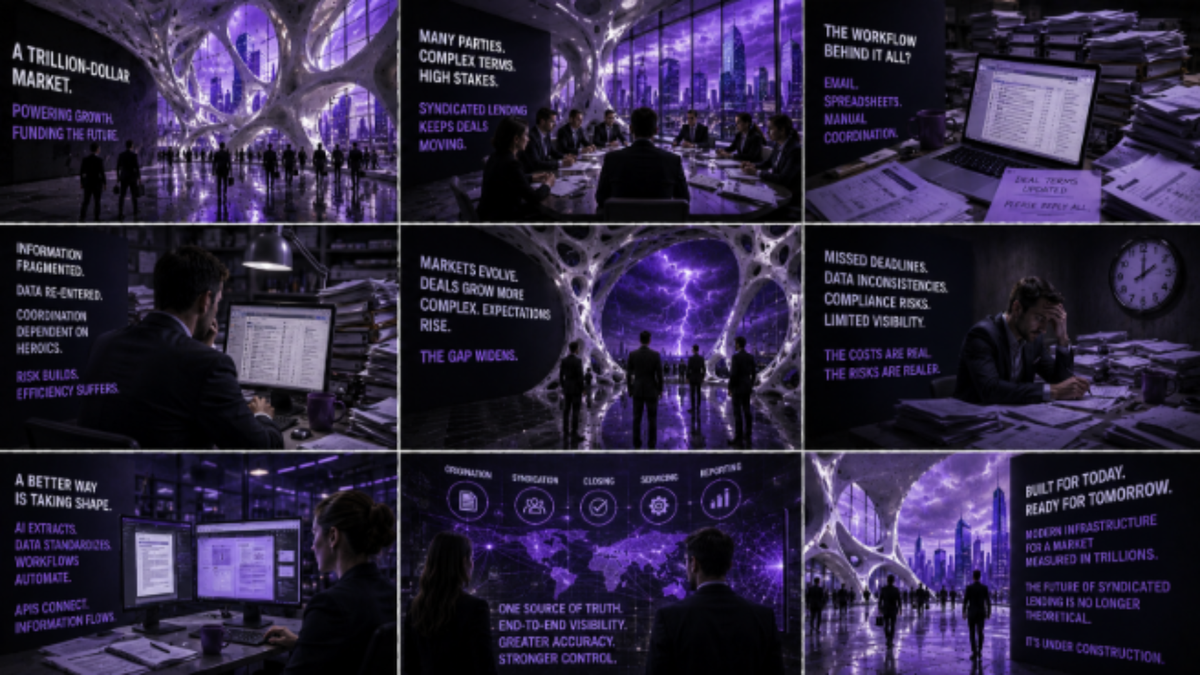

The Trillion-Dollar Syndicated Lending Market Still Runs on Email

Syndicated lending moves trillions of dollars annually and still runs on email and spreadsheets. Here is what that costs the market and what is starting to change.

Author: Karen Slagle, Senior Product Specialist at Lamina.

Syndicated lending is one of the most important, and least visible, engines of U.S. finance. Annual syndicated loan issuance often exceeds $1 trillion, funding everything from leveraged buyouts to corporate expansion and infrastructure projects. As private credit continues to grow, the boundary between syndicated markets and private credit is becoming increasingly fluid, with both markets competing for deals, refinancing one another, and sharing investors and risk across the broader credit ecosystem.

Each transaction involves multiple parties, including lead arrangers, lenders, agents, and borrowers, all coordinating across timelines, obligations, and evolving deal terms.

What is often overlooked is that many of these workflows still rely heavily on email, spreadsheets, and manual coordination across the full loan lifecycle — from origination and syndication through closing and ongoing servicing.

Rethinking the Backbone of Syndicated Lending

The syndicated lending market has long operated through a patchwork of inboxes, spreadsheets, and institution-specific processes. For years, this approach was viewed as workable. Experienced teams built internal systems and operational workarounds that allowed transactions to move efficiently enough in practice.

But as deal volume increases and structures become more complex, the limitations of these workflows are becoming harder to ignore.

Information is frequently fragmented across email threads and disconnected systems.

Key data points are manually re-entered multiple times. Coordination often depends more on individual institutional knowledge than on standardized processes. What once functioned adequately at smaller scale is now creating operational friction across the lifecycle of a deal.

When workflows remain tied to unstructured communication, it becomes increasingly difficult to standardize data, maintain visibility across participants, or scale efficiently as activity grows.

Where the Model Starts to Break Down

The strain is particularly visible in areas such as notice distribution and ongoing deal administration, where timing and accuracy are critical. But these issues reflect a broader structural challenge: the lack of connected, system-driven workflows linking each stage of the lending lifecycle.

As a result, firms often operate with limited transparency into where information resides, how it has been interpreted, and whether it has been consistently applied across participants. This can create downstream risks not only in execution, but also in reporting, compliance, and investor communications.

At the same time, the market itself is evolving. Private credit continues to expand, deal structures are becoming increasingly bespoke, and expectations around speed, transparency, and auditability are rising. The gap between how the market operates and what the market now requires is widening.

A Shift Toward More Structured Workflows

Across the market, there are early signs of a gradual shift away from inbox-driven coordination toward more structured, system-based workflows.

Advances in AI-driven data extraction are making it easier to capture and standardize information directly from notices and transaction documents, reducing manual interpretation and improving consistency across participants. Processes that were once considered too variable to automate are becoming increasingly manageable.

At the same time, API-based infrastructure is improving connectivity between systems, reducing the need for repetitive manual entry and allowing information to move more consistently across platforms.

Rather than relying on individuals to manually interpret and distribute information, these workflows can help standardize and route data more efficiently across institutions and systems. The potential benefits extend beyond operational efficiency, supporting greater visibility, accuracy, and scalability across the full lifecycle of a loan.

Why Change Has Been Slow

None of these operational challenges are new. The limitations of email-based workflows have been widely understood across the market for years. The more difficult issue has been finding practical ways to address them.

Syndicated lending does not lend itself easily to standardization. Each deal is negotiated individually, documentation varies significantly, and even routine lender notices often lack consistent formatting or shared taxonomies across institutions.

That variability has historically limited automation efforts. Rule-based systems struggle with exceptions and in syndicated lending, exceptions are common.

There is also a coordination challenge inherent to the market itself. Lending transactions involve multiple counterparties, meaning that even if one institution modernizes internally, it still depends on other participants that may continue operating through legacy workflows.

What Comes Next

Syndicated lending is unlikely to transform overnight. The complexity of the market all but guarantees that change will be incremental.

But the direction of travel is becoming clearer.

The question is no longer whether these workflows will evolve, but how quickly institutions can transition toward more structured and connected systems capable of supporting the full lifecycle of a loan.

For firms operating at scale, across banking, private credit, and syndicated lending alike, the priority is increasingly pragmatic: identifying where manual processes create the greatest operational risk, improving visibility where possible, and building infrastructure that can support more consistent and scalable execution.

Because for a market measured in trillions, reliance on the inbox was never designed to be permanent, even if it lasted longer than many expected.

About the author

Karen Slagle is a Senior Product Specialist at Lamina, a West Monroe company focused on improving the speed, efficiency, and transparency of syndicated and participation lending operations.

With deep experience in syndicated commercial lending, she specializes in middle- and back-office support for complex syndicated and participated loan facilities. She advises financial institutions on automating and digitizing syndication workflows and loan accounting notice processes, helping align front-office strategy with scalable, efficient downstream operations.