SpaceX IPO: $135 Per Share, $75 Billion Raised, and a $1.77 Trillion Bet on What Orbit Becomes Worth

SpaceX priced its IPO at $135 per share on June 11, listing on Nasdaq as SPCX on June 12. Here is what the deal structure and the financials actually say.

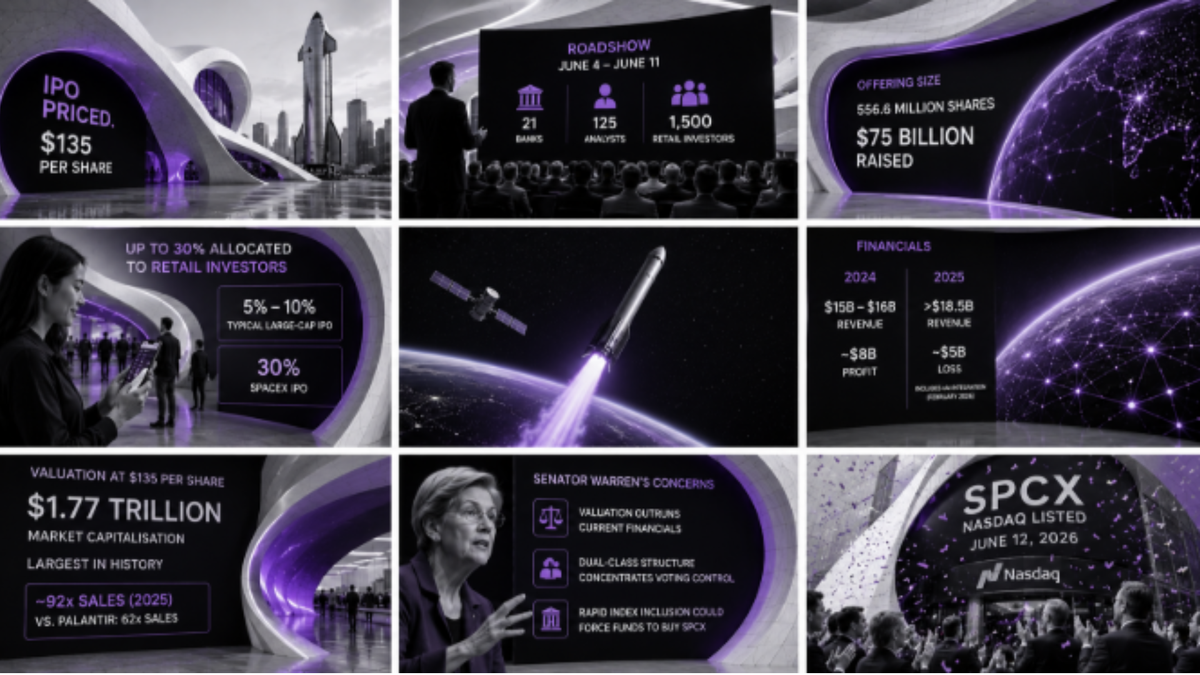

Space Exploration Technologies Corp., known as SpaceX, priced its initial public offering (IPO) at $135 per share on the evening of June 11, setting a June 12 debut on the Nasdaq under the ticker SPCX. With approximately 13.1 billion total shares outstanding, that price implies a market capitalisation of $1.77 trillion — the largest in the history of public markets. The offering covers 556.6 million shares, raising $75 billion in a single transaction.

What the deal structure looks like

SpaceX confidentially filed its draft registration statement with the US Securities and Exchange Commission (SEC) on April 1, 2026, and published its S-1 prospectus publicly on May 20 — satisfying the SEC's requirement to file at least 15 days before a roadshow. The roadshow launched on June 4, ahead of the originally planned schedule, after the SEC completed its review faster than anticipated. Approximately 125 analysts from 21 banks participated, alongside a dedicated session for around 1,500 retail investors on June 11.

The retail allocation is one of the more structurally unusual features of this offering. SpaceX set aside up to 30% of shares for retail investors, compared with the 5% to 10% typical in standard large-cap listings. For context, anyone who wanted exposure to SpaceX before today had two routes: secondary market transactions at steep minimums, or the tokenized equity access offered by platforms including Bybit and Kraken, which gave crypto users access to the IPO price through blockchain-settled instruments. The direct retail tranche puts a share in a standard brokerage account for the first time in the company's 24-year history.

What the financials actually show

SpaceX reported revenue of approximately $15 billion to $16 billion in 2024, alongside roughly $8 billion in profit, according to Reuters reporting from January 2026 citing the company's internal figures. The 2025 picture is materially different. Revenue exceeded $18.5 billion for the year, but the company posted a loss of nearly $5 billion — a reversal attributed largely to the integration of xAI, Elon Musk's artificial intelligence venture, which SpaceX acquired in February 2026. Starlink, the satellite broadband division, generated an estimated $10 billion of that 2025 revenue and produced around $6 billion in earnings before interest, taxes, depreciation, and amortisation (EBITDA) from core launch and satellite operations.

The valuation at $135 per share prices SpaceX at approximately 92 times its 2025 sales — a multiple that exceeds Palantir Technologies, currently the most expensively valued stock in the S&P 500, at 62 times sales. Morningstar has estimated SpaceX's fair value at $780 billion, implying a gap of roughly $990 billion between that estimate and the IPO price.

What the market is actually pricing

Starlink is the commercial engine behind any near-term valuation case. By late 2025, the service had reached an estimated seven to eight million users, with revenue growing across residential, enterprise, maritime, and aviation segments. The direct-to-cell service, which routes connectivity through standard mobile handsets without ground infrastructure, adds a further growth vector that analysts have not yet fully modelled. Falcon 9, the reusable launch vehicle that completed over 138 missions in 2024, generates the cash that funds everything else.

Starship, the heavy-lift system designed for lunar cargo, Mars missions, and high-volume satellite deployment, has not yet reached commercial operation. The market at $1.77 trillion is pricing Starship at scale, Starlink at hundreds of millions of subscribers, and orbital access priced the way cloud computing priced data storage — as infrastructure with compounding returns as volume grows. Whether that future arrives on a schedule that justifies today's price is the only question the IPO cannot answer.

What Senator Warren raised before pricing

Around June 10, Senator Elizabeth Warren sent a letter to the SEC requesting a delay to the offering. Her concerns covered three areas: that the valuation outruns the current financials, that the dual-class share structure concentrates voting control with Elon Musk, and that rapid index inclusion could compel retirement and index funds to purchase SPCX regardless of their holders' preferences. A senator's letter carries no regulatory authority to halt an IPO. The SEC reviews disclosures and compliance, not whether a price is fair, and the offering proceeded on schedule.

What this listing changes for capital markets

The size of the retail tranche, the use of tokenized instruments to pre-position crypto-native investors before the S-1 was public, and the governance structure of the dual-class share model are features that sit at the centre of current financial technology and public markets reform. The 30% retail allocation, if it becomes a reference point for future large-cap listings, changes the economics of who gets access to IPO pricing — a question that fintech infrastructure has been circling without a direct test at this scale. Tomorrow is that test.

Editor's note

Every piece published on The Bright Minded goes through careful verification, but mistakes can happen. If you spot an error, have additional information, or want to flag anything, write to rosalia@thebrightminded.com.