Jamie Dimon Says the CLARITY Act Is Dead on Arrival. His Own Bank Tells a Different Story.

JPMorgan CEO called the CLARITY Act dead on arrival. The same bank runs a blockchain unit actively building what it calls a digital alternative to stablecoins.

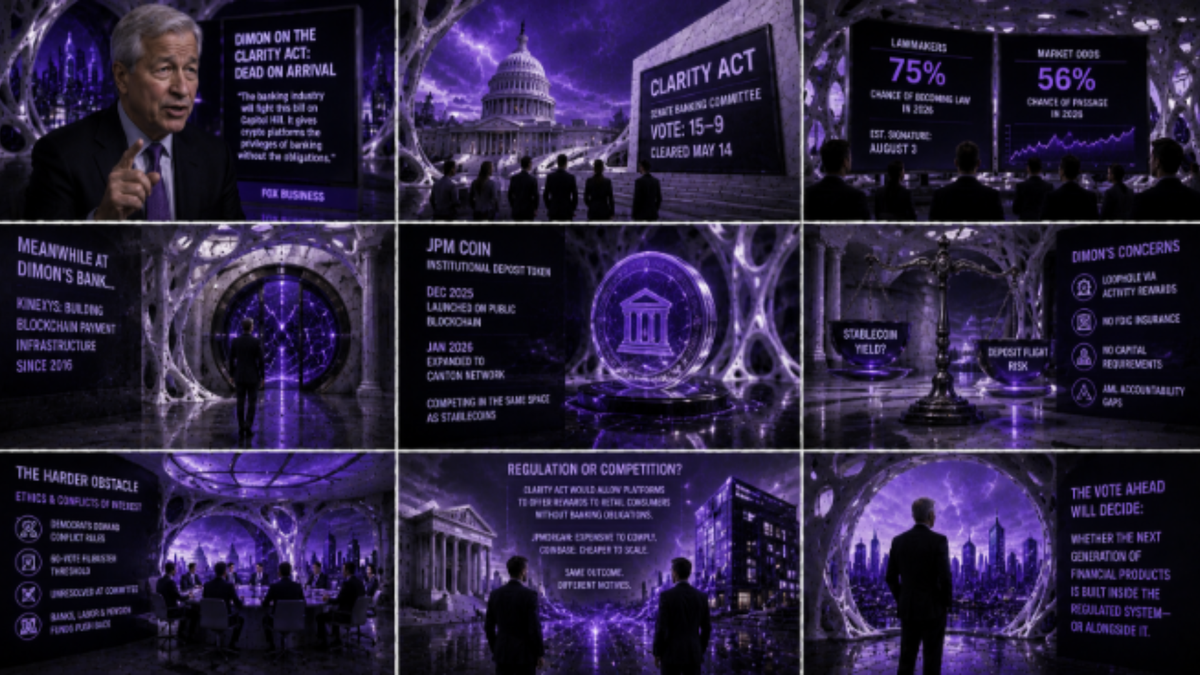

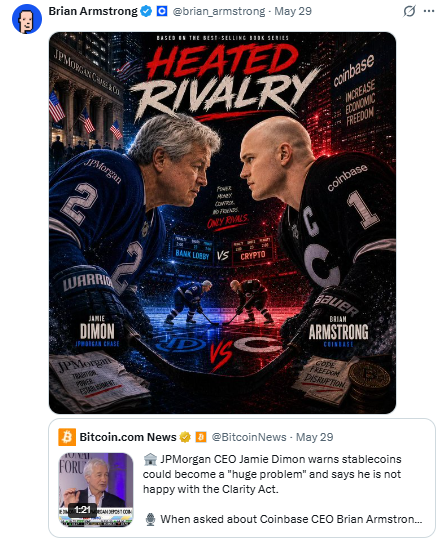

Jamie Dimon appeared on Fox Business on May 29 to say the CLARITY Act, the crypto market structure bill currently heading toward a Senate floor vote, would be dead on arrival if Congress passed it unchanged. He pledged that the banking industry would fight it on Capitol Hill, accused Coinbase CEO Brian Armstrong of spending hundreds of millions in lobbying to push it through, and argued that the bill hands crypto platforms the privileges of banking without the obligations.

Armstrong responded on X on May 29 with a mocked-up hockey rivalry poster, labelling the matchup "Bank Lobby vs Crypto" and framing it as JPMorgan against Coinbase.

JPMorgan's blockchain unit, Kinexys, has been building payment infrastructure on distributed ledger technology since 2016. Its deposit token, JPM Coin, moved to a public blockchain in December 2025 and expanded to the Canton Network in January 2026, making it available beyond JPMorgan's direct institutional clients to external counterparties.

JPMorgan describes JPM Coin on its own product pages as an institutional deposit token designed to compete in the same space as stablecoins. Dimon's objection to the CLARITY Act centres on stablecoin yield. His bank has been building the competing infrastructure for nearly a decade.

What Dimon said and why it matters now

Dimon's core objection in the Fox Business interview is the one banks have raised since the stablecoin yield compromise brokered by Senators Tillis and Alsobrooks emerged in early May: that banning passive yield while permitting activity-based rewards creates a loophole wide enough to drive deposit flight through.

A stablecoin paying rewards for platform activity is, in his argument, functionally equivalent to a savings account, and any institution offering one should carry FDIC insurance, capital requirements, and Bank Secrecy Act obligations. He also raised anti-money laundering concerns, warning that decentralised payment networks create accountability gaps that disappear once funds move outside the regulated banking perimeter.

Dimon told Fox Business that the banking industry has no intention of yielding to pressure from a single company, and that the sector's opposition would hold regardless of how much lobbying capital Coinbase deployed.

Where the bill stands and what the odds reflect

The CLARITY Act cleared the Senate Banking Committee with a 15-9 vote on May 14. Galaxy Research put the probability of the bill becoming law in 2026 at 75% after that vote, with a central estimate placing a presidential signature around August 3.

Polymarket, where traders put real money behind their predictions, sits at 55% as at the time of writing. The banking lobby's fracture along commercial lines ahead of the markup, with large retail deposit holders opposed and smaller institutions more willing to accept the compromise, is the same division Dimon's intervention reflects at the floor stage.

The obstacle that Dimon is not the loudest voice on

The stablecoin yield fight is the most visible argument around the CLARITY Act, but the ethics provisions present the harder obstacle on the floor. Democrats whose votes are required to clear the 60-vote filibuster threshold have conditioned their support on conflict-of-interest rules targeting elected officials with financial ties to the crypto industry. That demand was unresolved at committee. The ABA's coordinated pre-markup lobbying campaign and the pension fund exposure concerns raised by labour unions represent constituencies whose positions the bill has not yet resolved.

The competitive argument dressed as a regulatory one

JPMorgan's Kinexys processes blockchain-settled payments for institutional clients who already bank with JPMorgan. The CLARITY Act, if passed with activity-based rewards intact, would allow platforms like Coinbase to offer retail consumers a product that generates returns on digital balances, at scale, without the compliance infrastructure that makes JPMorgan's deposit operations expensive to run. The consumer protection argument and the competitive argument point in the same direction, and separating one from the other requires more than Dimon's Fox Business appearance offers.

Dimon told Fox Business that if the banking industry loses the fight in Congress, it will accept the result. The bill's floor vote will determine whether the next generation of financial products available to American consumers is built inside the regulated banking system or alongside it.

Editor's note

Every piece published on The Bright Minded goes through careful verification, but mistakes can happen. If you spot an error, have additional information, or want to flag anything, write to rosalia@thebrightminded.com.