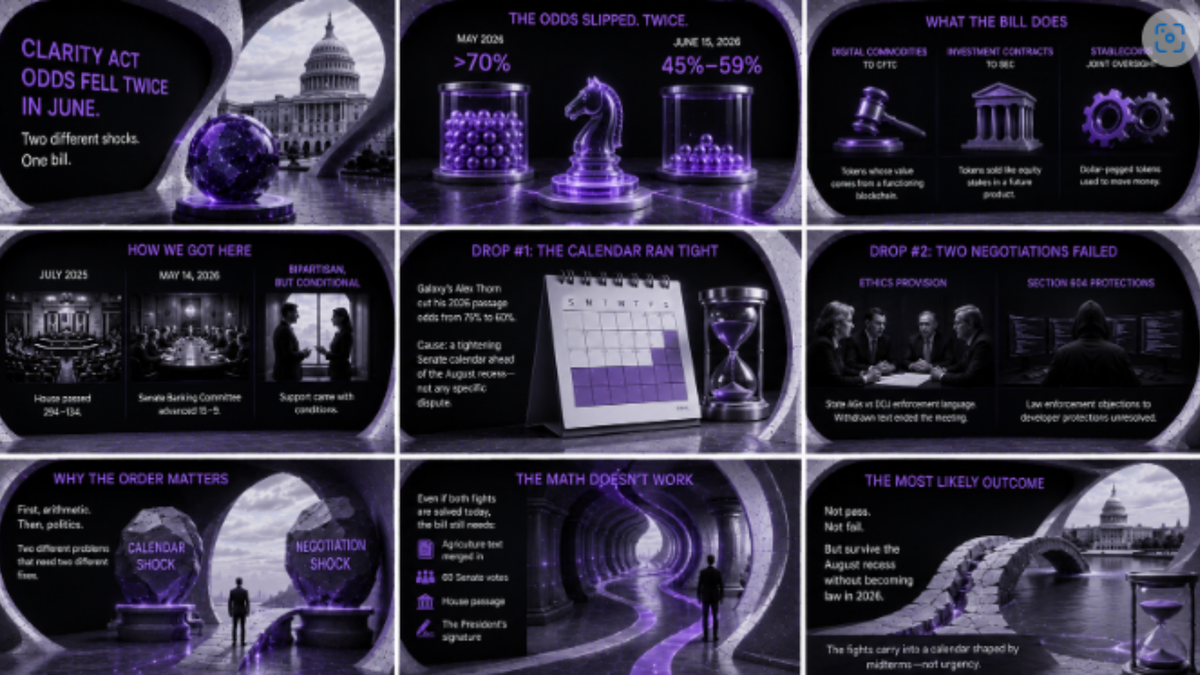

CLARITY Act Odds Fell Twice in June for Two Unrelated Reasons

CLARITY Act passage odds fell from 75% to 60% on the calendar alone, then to a coin flip after ethics and Section 604 talks both collapsed.

Prediction markets tracking the CLARITY Act priced the bill's passage above 70% in May. As of yesterday, the same markets sit between 45% and 59%, a range wide enough that traders themselves disagree on what is actually happening. The honest answer is that two separate things happened, not one.

The bill's confidence collapsed once because the Senate ran out of calendar room, and then again because two unconnected negotiations both failed.

Galaxy Digital's head of research, Alex Thorn, put a number on the first shock in a note lowering his 2026 passage estimate from 75% to 60%. He named the cause directly: a tightening Senate calendar ahead of the August recess, not any specific dispute breaking down. At that point, the stablecoin yield fight, the ethics provision, and illicit-finance language were all still open, but none of them had collapsed. The bill simply had less floor time than the optimism after committee had implied.

What the bill actually does, and how it got this far

The Digital Asset Market Clarity Act assigns a named federal regulator to every digital asset for the first time in US law. Tokens whose value comes from a functioning blockchain move to the Commodity Futures Trading Commission (CFTC) as digital commodities. Tokens sold like an equity stake in a future product stay with the Securities and Exchange Commission (SEC) as investment contracts. Dollar-pegged tokens used to move money receive joint oversight from both agencies, building on the stablecoin framework Congress passed through the GENIUS Act in 2025.

The House passed its version 294 to 134 in July 2025. The Senate Banking Committee advanced its own text 15 to 9 on May 14, 2026, with Senators Ruben Gallego of Arizona and Angela Alsobrooks of Maryland crossing over to supply the bipartisan margin. Both made their votes explicitly conditional on further work, conditions that have since hardened into the obstacles now stalling the bill on the floor.

The first drop was arithmetic, not anger

Thorn's June downgrade is worth separating cleanly from what came after it, because the two causes do not overlap. The calendar problem existed independently of any single fight. Even with every dispute resolved on the spot, the bill still needed its Banking Committee text merged with the separate Agriculture Committee framework covering CFTC jurisdiction, then floor time, then 60 votes, then House reconciliation, then a signature. Every one of those steps draws on session days the Senate floor calendar was no longer generously supplying. A bill can have genuine bipartisan support and still run short of room, in the same way a fully booked flight can still miss its slot if boarding simply takes longer than the gate allows.

Then two negotiations failed

The second shock arrived on a completely different axis. A closed-door meeting on the bill's ethics provision, bringing together Senators Kirsten Gillibrand, Gallego, Bernie Moreno, and Cynthia Lummis alongside White House crypto adviser Patrick Witt, ended without agreement when Republicans and the administration withdrew a specific piece of text: language that would have let state attorneys general sue the Department of Justice over failures to enforce conflict-of-interest rules tied to crypto holdings.

Gillibrand has staked her support on that kind of provision existing in some form. The White House has said it will not accept language that reads as targeting one officeholder. Each side is describing the same clause accurately, and that is precisely why withdrawing it closed the meeting instead of moving it forward.

The dispute sits downstream of how directly elected officials can be tied to criminal liability questions the bill raises elsewhere, which is part of why an apparently narrow enforcement mechanism carried enough weight to end the session.

A separate meeting addressing law enforcement's objections to developer protections under Section 604, the provision shielding non-custodial software developers from money-transmitter treatment, also ended without resolution. Senators Mark Warner and Catherine Cortez Masto have tied their floor votes to that fight specifically, distinct from the ethics dispute entirely. The bill now needs two separate pairs of senators to independently release two unrelated holds, not one pair to resolve one disagreement.

Eleanor Terrett, who has tracked this bill's negotiations closely, posted on June 15 that "the math doesn't work": even with the ethics language and the Section 604 language both settled immediately, the bill would still need the Agriculture Committee text merged in, 60 floor votes secured, and passage through both chambers, compressed into roughly two weeks. The same dynamic that pushed the SEC chair to make his public case for the bill from outside the usual regulatory venues now works against the administration's preferred deadline: signaling support does not create floor time.

Nevertheless, Rep. Dusty Johnson told that "If the Senate can get this done in the next few weeks, we will move fast.”

Why the order of the two failures matters

Collapsing this into one continuous slide, from 75% in May to the high 40s now, misses what actually happened. The calendar shock and the negotiation shock are not the same event measured at two points. They are two independent failures that landed inside the same six-week window, each capable of stalling the bill on its own. A calendar problem is something Senate leadership can solve directly, by finding floor time. A negotiation problem requires two separate pairs of senators to each decide, independently, that their condition has been met, which leadership does not control at all.

That distinction echoes a pattern already visible in how the banking lobby's opposition fractured along commercial rather than ideological lines earlier in the process. Disputes that look unified from the outside often turn out, on inspection, to be several distinct fights wearing one label, and each one needs its own resolution rather than a single compromise. Banks were even fighting the same battle in two venues at once, pressing an identical argument simultaneously at the Senate markup and at the OCC, which is the closest precedent the bill has for a single underlying disagreement splitting into parallel fronts that each demand separate attention.

The CLARITY Act's most likely outcome now, by the numbers research desks are publishing, is neither pass nor fail. It is the quieter third option: a bill that survives the August recess without dying, but also without becoming law in 2026, carrying both unresolved fights into a legislative calendar reshaped by midterm politics rather than legislative urgency.

A bill that loses its premium once for running out of time, and again for running out of agreement, has demonstrated something specific about its own fragility. It can fail in two unconnected ways at once. That is harder to recover from than failing in one, and it is a different problem than the one Jamie Dimon described when he called the bill dead on arrival. Dimon was describing opposition. What stalled the bill this month was not opposition. It was two good-faith disagreements that happened to need the same six weeks to resolve, and ran out of weeks before either one did.

Editor's note

Every piece published on The Bright Minded goes through careful verification, but mistakes can happen. If you spot an error, have additional information, or want to flag anything, write to rosalia@thebrightminded.com.