UK Buy-Now, Pay-Later Regulation: The Rules Work by Making Shoppers See It as Debt Again

UK Buy-Now, Pay-Later rules are now in force under the FCA. The biggest change is not affordability checks, it is that the product is finally labelled as credit.

The Bright Recap

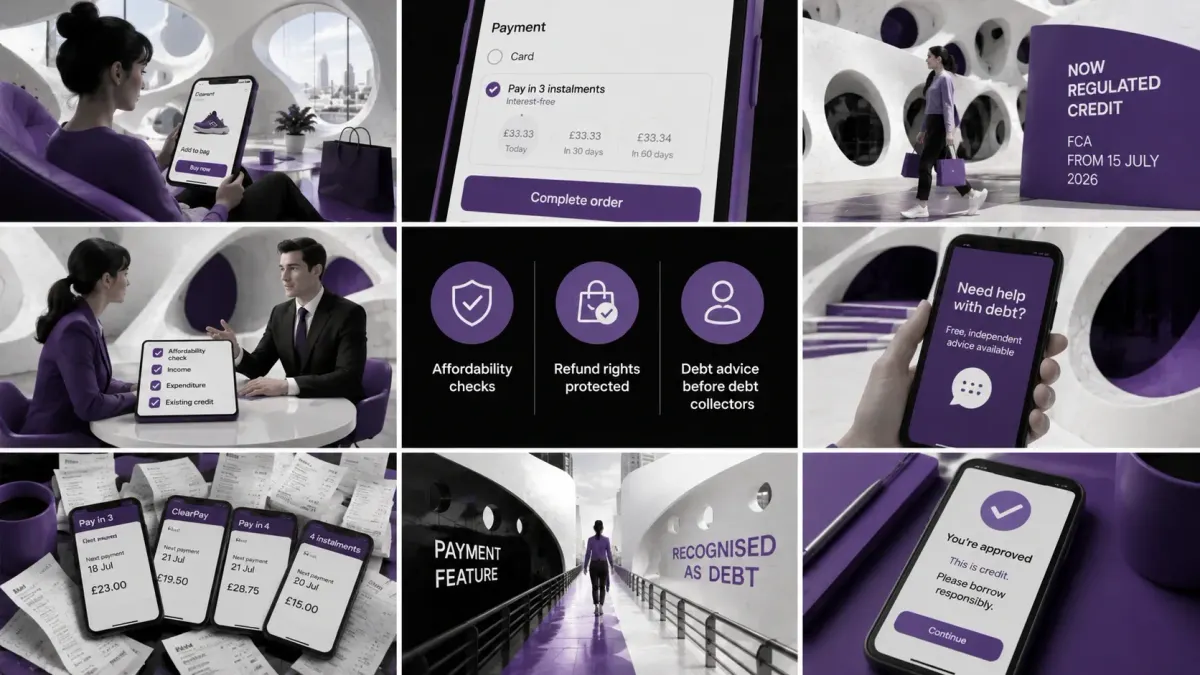

UK Buy-Now, Pay-Later rules came into force on 15 July 2026, placing the sector under Financial Conduct Authority (FCA) oversight. Providers such as Klarna, PayPal and Clearpay must now run affordability checks before offering credit, give clear refund rights on faulty goods, and route users in difficulty to debt advice rather than a debt collector.

To know more about this topic, read our related articles:

- How tools reshape money decisions

- When credit access outruns protection

- What the FCA watches in payments

- Financial technology explained

Bright Answers

What changes for Buy-Now, Pay-Later users in the UK?

Providers must check that a purchase is affordable before approving it, users gain enforceable refund rights on faulty goods, and anyone in financial difficulty is pointed to debt advice first. Complaints can now go to the free Financial Ombudsman Service.

Will most people notice a difference?

Probably not at checkout. The protections mainly matter when something goes wrong, such as a wrongly marked credit file or a product sold without being explained as a debt. Responsible users should see little added friction.

Buy-Now, Pay-Later worked so well partly because millions of people using it did not fully register that they were borrowing. A payment split into three interest-free instalments at online checkout feels like a feature of the shop rather than a loan from a lender. From 15 July 2026, that product is regulated credit in the United Kingdom, overseen by the Financial Conduct Authority (FCA), and the most consequential thing the new rules do is put the word debt back in front of the person clicking the button.

The measures themselves are real and worth stating plainly, since providers such as Klarna, PayPal and Clearpay must now check that a shopper can afford a purchase before approving it. Refund rights on faulty goods have been brought into line with those on any other regulated credit product, and a customer who falls behind is directed to debt advice instead of a debt collector.

This story was Elevated by Cantica's Purgatorio.

Cantica is the Fin-Tech intelligence system behind The Bright Minded.

The honest good this does

One protection stands out for the people who need it most, because anyone treated unfairly can now take a complaint to the Financial Ombudsman Service, a free and independent body, without hiring anyone or going to court. A wrongly marked credit file, or a product pushed without being explained as a debt, becomes something a person can escalate at no cost. For a household without the money to fight a dispute, a free route to an independent decision is a genuine shift in power, and it is the part of this package most likely to change an individual outcome.

The affordability checks matter as well, though more quietly. The government has been careful to say responsible users should notice little added friction, which is the honest framing, because the checks are aimed at the account quietly opening a fourth or fifth agreement rather than the person making a single considered purchase.

The reclassification is the real intervention

The deeper change is definitional, since for most of its growth Buy-Now, Pay-Later sat outside the consumer credit rules that govern a credit card or a personal loan. A shopper using it had fewer rights on the same item than a shopper who paid with plastic. Bringing it under the FCA closes that gap in law, and it also closes a gap in perception, because a regulated credit product has to present itself as one.

Consumer advocates have been direct about why this matters. The campaigner Martin Lewis has pointed out that a large share of users do not recognise the arrangement as debt at all, which is what made it unsafe for some of them. StepChange, a debt charity, notes that people who use these products are considerably more likely to be dealing with debt problems already. The behavioural risk was never the interest, since there usually is none, and instead it was a form of borrowing that did not feel like borrowing, accumulating across several apps at once.

Why a payment feature became a debt nobody counted

The design is where the phenomenon lives, because a credit card statement arrives once a month and shows a single balance, which is a moment of reckoning however unwelcome. Buy-Now, Pay-Later spreads the same borrowing across separate purchases, separate providers and separate repayment dates, so no single screen ever shows the total. A person can hold six live agreements and never see the sum of them in one place.

This is the same pattern that appears whenever a piece of financial technology removes a point of friction that also served as a moment of awareness, much as everyday money tools have started to change small financial decisions for people who never sought advice. Smoothness is the product, and regulation reintroduces a measure of the friction that the product was built to erase, in the form of a check, a disclosure and a clear label.

What regulation reaches and what it does not

The rules meet a timing question that has run in the opposite direction elsewhere, since the United Kingdom is tightening protection around consumer credit at a moment when other jurisdictions have widened access to credit faster than protection. That contrast is a fair way for a reader to judge what this choice is worth. The FCA is the same regulator already examining how competition works inside digital payments, so the sector now answers to a body with a view of the wider plumbing.

An affordability check can refuse a loan that cannot be repaid, and it cannot make a person feel the weight of a debt split into small, cheerful instalments, which was always the thing keeping spending in check. The rules give people rights they lacked yesterday, and their quieter achievement is to make a shopper pause long enough to notice that the pay-later button is a lender asking a question.

Editor's note

Every piece published on The Bright Minded goes through careful verification, but mistakes can happen. If you spot an error, have additional information, or want to flag anything, write to rosalia@thebrightminded.com.