Sterling Has $1.53 Million in a $315 Billion Stablecoin Market. The Lords Just Explained Why

The House of Lords published its stablecoin report on 3 June. Sterling's entire stablecoin market is worth $1.53 million. Here is what that number reveals.

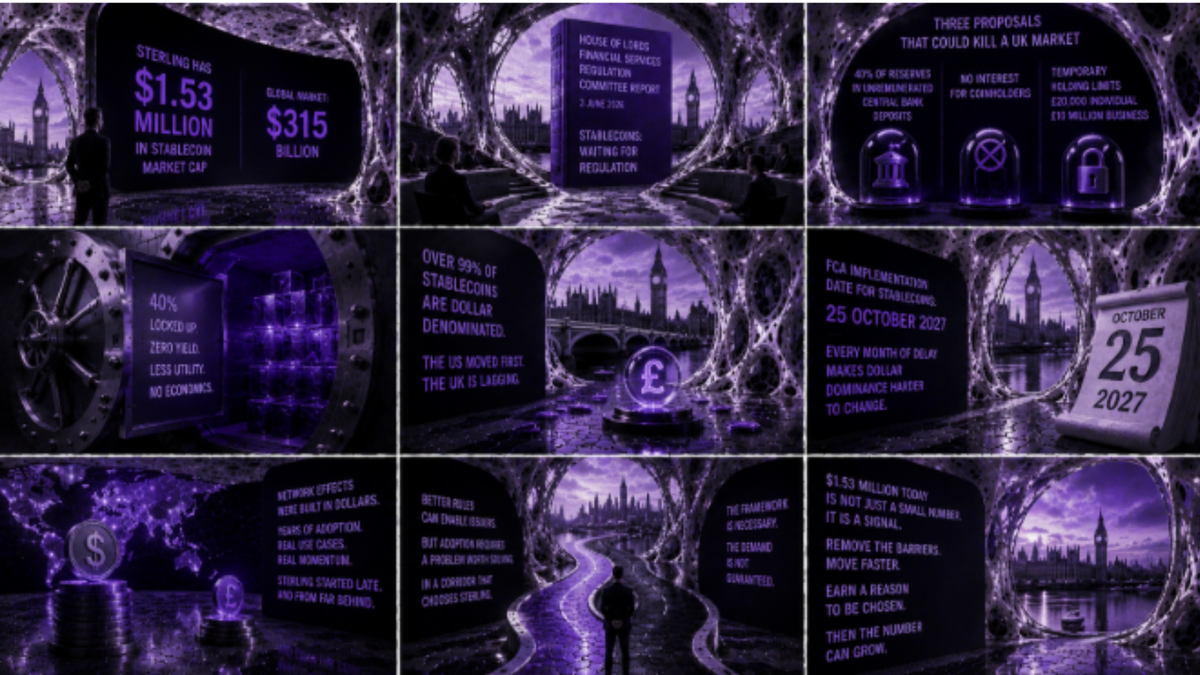

Sterling has $1.53 million in stablecoin market cap. The global market is worth $315 billion. Both figures appear in the House of Lords Financial Services Regulation Committee report published on 3 June 2026, and together they tell a more precise story than anything else in the committee's 71 pages.

The report, titled Stablecoins: waiting for regulation, examined the Bank of England and FCA's proposed frameworks for UK stablecoins after a five-month inquiry. The committee broadly endorsed both frameworks. It also flagged three specific BoE proposals it concluded would make a sterling stablecoin commercially unworkable before any issuer had built a viable product, and called for each to be reconsidered before the Bank publishes revised draft rules later this month.

What the Bank of England proposed

In November 2025, the Bank of England published its consultation paper on a regulatory regime for sterling-denominated systemic stablecoins. Systemic refers to stablecoins used widely enough in retail payments to pose potential risks to financial stability, a threshold no sterling stablecoin currently approaches.

The paper proposed that systemic issuers hold at least 40% of backing assets in unremunerated central bank deposits, that coinholders receive no interest, and that temporary holding limits of £20,000 per individual and £10 million per business apply during an initial transition period.

The 40% reserve requirement drew the sharpest criticism from industry respondents to the inquiry. Parking nearly half of all backing assets in a non-interest-bearing central bank account erodes the economics of issuing a sterling stablecoin from day one.

The Lords committee found the requirement poorly calibrated, concluding it could carry serious consequences for the commercial viability of UK stablecoin issuers, and called for a less prescriptive, principles-based approach to backing asset composition. On holding limits, the committee said the Bank should refrain from imposing any caps at all during the early stage of market development, monitoring conditions and acting only if financial stability risks make intervention clearly necessary.

Bank of England Deputy Governor Sarah Breeden had already acknowledged in May, ahead of the Lords report, that the proposals were overly conservative and that the Bank was re-examining its approach to the risks involved.

Dollar dominance and the competitive context

Over 99% of the global stablecoin market is denominated in US dollars, with Tether and Circle accounting for around 90% of that total, according to the Lords report. The US established a federal framework for dollar-backed stablecoins through the GENIUS Act before the UK's full cryptoasset regime, including stablecoins, is even scheduled to come into force. The FCA's implementation date is 25 October 2027. The euro's dollar problem required a coalition of 37 banks to attempt a collective answer, and that effort is still in progress.

The Lords committee characterised the UK as lagging behind both the US and EU, warning that commercially unworkable rules and further delay risk cementing dollar dominance in sterling payment corridors. The concern is well-founded. It also captures only part of what the $1.53 million figure shows.

What the number predates

tGBP's $1.53 million market cap existed before the BoE published its November 2025 consultation. The holding caps, the 40% reserve requirement, the interest ban — all came after sterling stablecoins had already failed to attract meaningful adoption. Sterling's near-absence from this market reflects a currency that has not established itself in the payment corridors where stablecoin use became self-sustaining: cross-border remittances, crypto-native settlement, gig economy payments across borders. Those corridors were built on dollars, through years of organic adoption that preceded any regulatory framework anywhere.

The UK regulatory calibration problem is real. Rules that are too restrictive to attract issuers, arriving too slowly to build market confidence, compound an existing disadvantage. The Lords identified this accurately. Removing the commercial barriers the BoE's proposals create is the right step.

Beyond the framework

Regulatory certainty gives issuers the conditions to build. It does not generate the network effects that make a payment instrument worth using. A stablecoin's utility grows with adoption, and adoption in this market has historically followed genuine demand in specific communities, not the publication of a framework. Europe's stablecoin bet showed what happens when rules arrive ahead of demand: MiCA gave euro stablecoins a credible legal foundation, and the market then discovered the harder work of competing with dollar-denominated infrastructure that users already trusted.

Sterling faces the same challenge from a smaller base. The Lords report is the right intervention, correctly targeted at the rules that would have made issuance uneconomical before it started. The question the report does not answer is which specific population, in which payment corridor, has a problem that a sterling stablecoin solves better than the dollar alternatives already in use. A currency that has not answered that question at $1.53 million will not find the answer automatically at a larger number.

Editor's note:

Every piece published on The Bright Minded goes through careful verification, but mistakes can happen. If you spot an error, have additional information, or want to flag anything, write to rosalia@thebrightminded.com.