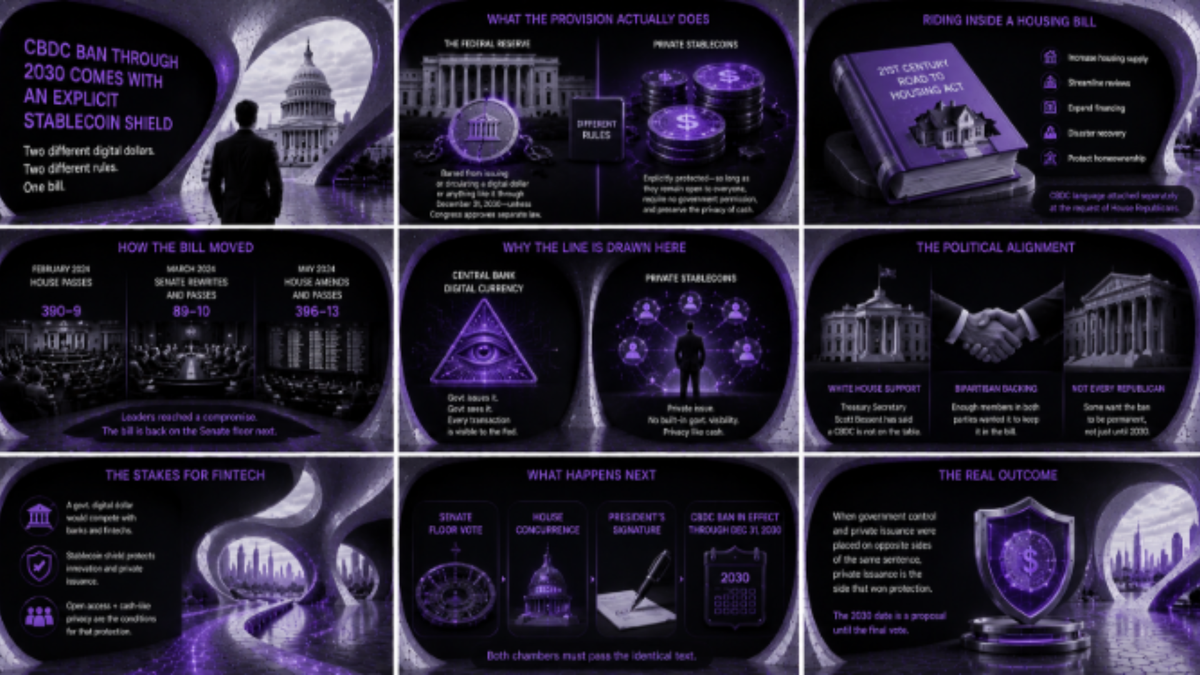

CBDC Ban Through 2030 Comes With an Explicit Stablecoin Shield

A digital dollar ban running through 2030 protects stablecoins by name, the clearest signal yet of which side of crypto policy Washington has chosen.

The Federal Reserve would be barred from issuing anything resembling a central bank digital currency through the end of 2030 without separate congressional approval, while the private stablecoins doing largely the same economic job, moving dollar value digitally, get an explicit carve-out protecting them by name, so long as they preserve the privacy a person gets from holding physical cash.

That distinction is the actual policy outcome inside H.R. 6644, the 21st Century ROAD to Housing Act, a bill whose name gives no hint that it touches digital currency at all. Its core purpose is increasing housing supply, with provisions streamlining environmental review requirements, expanding financing for manufactured homes, funding disaster recovery, and barring large institutional investors from buying up single-family homes.

The central bank digital currency language was attached separately, at the request of House Republicans, with no structural connection to housing policy. It stayed in the bill because enough members wanted it there on its own merits to keep it attached through multiple rounds of negotiation.

A fintech question riding inside a housing bill

What the provision actually does is worth stating plainly, since the legal language itself is dense. The Fed would be prohibited from creating or putting into circulation a government-issued digital dollar, or anything functioning like one, for the next several years, unless lawmakers pass a separate law authorizing it.

Sitting in the same clause, the bill explicitly protects a different category of digital dollar entirely: privately issued tokens, the kind fintech companies and crypto firms already issue and that trade under names like USDC or USDT, are carved out from the restriction as long as they remain open to anyone, require no government permission to use, and keep the same privacy a person already has when paying with a banknote.

The legislation has already passed both chambers twice, in two different forms

The House passed an earlier version in February by 390 to 9. The Senate then substantially rewrote that bill, adding the digital currency language along with other provisions, and passed its version in March by 89 to 10. The House amended the Senate's text again and passed that version in May by 396 to 13. What happened then was committee leaders agreeing on compromise language meant to let the Senate take up the House's changes and move toward a version both chambers can finally pass without further edits. That puts the bill back on the Senate floor next, not the House, and both chambers still need to agree on identical text before anything reaches the president.

To reach this compromise, the Senate accepted a shorter window on a disaster-recovery grant program, while taking on House-favored provisions including several community banking measures and the institutional-investor restrictions. The committee leaders behind the deal, from both parties and both chambers, have each pointed to different pieces of the bargain as the part that justified the trade, the housing supply measures on one side, the dozens of additional provisions added during negotiation on the other.

Why the line landed exactly where it did

The CBDC ban isn't new to this week. The Senate first attached it back in March, and the White House backed the idea around the same time. Treasury Secretary Scott Bessent has separately and repeatedly said a government-issued digital dollar isn't something this administration is considering, independent of whatever Congress eventually does with this bill. That alignment between the legislative language and the administration's own stated position is a meaningful part of why the provision survived several rounds of rewriting largely intact.

Not every Republican thinks a 2030 expiration date goes far enough. Representative Anna Paulina Luna has argued for making the prohibition permanent rather than letting it lapse on a fixed date, on the theory that the risks of a government-controlled digital currency don't disappear just because a particular administration currently opposes one. That disagreement sits inside one party rather than across the aisle, and it remains one of the open questions that could still shape how cleanly the bill clears its remaining votes.

The structural reason the bill treats a Fed-issued digital dollar and a privately issued stablecoin so differently comes down to who can see what. A central bank digital currency would put the Federal Reserve in direct technical contact with every digital dollar in circulation, since the central bank itself would issue and track it. A stablecoin is issued by a private company and pegged to the dollar's value, with no equivalent government visibility built into every transaction by design. The privacy language attached to the stablecoin carve-out exists specifically because that distinction, not the underlying technology, is what the debate has actually been about.

The bill still needs to pass the Senate and then the House in identical form before it reaches the president's desk, and the administration has signaled it would sign the package once that happens. Until both chambers vote again, the 2030 date is a proposal rather than law. But the shape of the compromise is already visible, and it answers the question crypto policy has been circling: when government control and private issuance were placed on opposite sides of the same sentence, private issuance is the side that won protection.

Editor's note

Every piece published on The Bright Minded goes through careful verification, but mistakes can happen. If you spot an error, have additional information, or want to flag anything, write to rosalia@thebrightminded.com.