The State of Fin-Tech Report June–July 2026

The June-July 2026 fin-tech market by Cantica, The Bright Minded's fin-tech intelligence layer: $2.67B disclosed capital, 61% buying automated finance, SpaceX perps at $7.1B, and a licensing race across four jurisdictions.

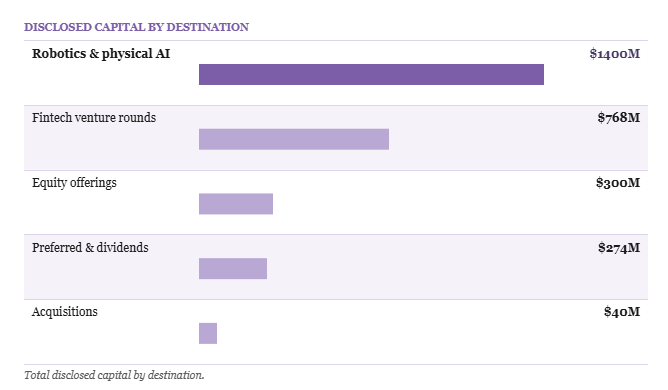

Fintech's disclosed capital between 7 June and 11 July 2026 came to $2.67 billion, and one transaction accounts for half of it. Tether led a Series C round of up to $1.4 billion in NEURA Robotics, among the largest physical artificial intelligence financings on record, stating its purpose as building the financial and intelligence layer of the robotics economy. Sorted by what the money buys, $1.64 billion of the total went into systems that transact with no person present.

The pattern holds across the period. Venture capital, the payment networks, the exchanges and the central banks all moved on the same question, which is what happens to finance when software becomes the counterparty.

This report was built on Cantica, The Bright Minded's Fin-Tech intelligence layer.

The funding market

Venture and growth rounds drew $655 million across 17 companies with disclosed round sizes. Taktile took the largest at $110 million in a Goldman Sachs-led Series C to automate credit and risk decisions inside financial institutions. Databento raised $97 million from NEA for market data feeds, Addi took $85 million from Citius and BTG Pactual for consumer credit in Latin America, and EDX Markets closed $76 million from SBI Holdings for its institutional digital asset exchange.

The five largest rounds account for 66 per cent of disclosed round capital, and the twelve beneath them average $18.6 million each. Scored on the Herfindahl-Hirschman Index, the standard measure of market concentration, these rounds return 1,032. Anything below 1,500 is a competitive market, so no group of investors or recipients holds a controlling position.

Largest Disclosed Fintech Venture Rounds

| Company | Round | What it builds, and who led |

|---|---|---|

| Taktile | $110M | Automated credit and risk decisioning inside financial institutions. Series C, Goldman Sachs |

| Databento | $97M | Market data feeds for automated systems. Series B, NEA |

| Addi | $85M | Consumer credit, Latin America. Series D, Citius and BTG Pactual |

| EDX Markets | $76M | Institutional digital asset exchange. Series C, SBI Holdings |

| Arca | $64M | Wealth management at scale. Stage and lead investor not disclosed |

| 12 further rounds | $223M | $18.6M average round. Largest is 5.9x this figure. |

$655 million across 17 companies with round sizes disclosed in US dollars, 16 June to 9 July 2026.

Two further rounds: Float Financial (CAD 85 million, Series C) and Wultra (€6.8 million, Series A).

What the smaller rounds bought is a useful signal. Tangos raised $20 million to run financial crime investigations with autonomous artificial intelligence, GrailPay took $10.5 million for risk decisioning infrastructure, and Orthogonal raised $4.3 million for agent service discovery and payments. Wultra raised €6.8 million for post-quantum digital security, the first sign in this data that quantum-resistant authentication has become a funded category.

Agentic commerce arrives at the card networks

Visa partnered with OpenAI on 10 June to build the payment layer for artificial intelligence commerce. Visa then published a Trusted Agent Protocol and an Agentic Directory, with Cleverbridge among the first merchants to enable them, and Nuvei completed a first-party payment executed by an agent through Visa on 2 July. The card networks have moved from describing agentic payments to processing them inside a single period.

The interface layer standardised at the same time. Webull launched a Model Context Protocol server allowing investors to trade in plain language, Lili brought one to accountants, and Navan applied the same open standard to travel and expense. Interactive Brokers added both ChatGPT and Grok to its platform on 22 June. A common protocol for letting language models act on financial systems was adopted across brokerages, neobanks and expense platforms before any regulator ruled on it.

Agentic commerce and artificial intelligence in financial services

Market structure

Crypto exchanges built a derivatives market on a company with no public listing. SpaceX perpetual futures became Binance's second most traded product, with the exchange capturing more than 60 per cent of the market. MEXC reported cumulative SpaceX futures volume above $7.1 billion by 30 June. Kraken launched perpetual futures for US clients, and Ondo opened the first equity perpetuals platform collateralised by tokenised stock.

The Commodity Futures Trading Commission opened a public consultation on 22 June covering perpetual futures and the extension of standard futures contracts to round-the-clock trading. A regulator is now consulting on the instrument these venues have already built and scaled.

Tokenised equities passed a threshold of their own. Ondo Global Markets surpassed $1 billion in total value locked, a first for tokenised stocks, and pushed distribution onto Hyperliquid, Uniswap, LI.FI and Ledger wallets across the period. Binance launched bStocks with one-to-one backing and round-the-clock trading, and SS&C added digital cash settlement to its tokenised investment range.

Passive capital opened a channel into crypto-linked equities. TAO Synergies, Canton Strategic Holdings and Hyperliquid Strategies entered Russell indices at the June reconstitution, alongside the identity verification firm Intellicheck. Index membership routes allocator money into these companies with no allocator deciding to buy the exposure.

Regulation

Europe's crypto licensing regime resolved. Ripple secured preliminary authorisation under the Markets in Crypto-Assets regulation on 23 June and full authorisation on 6 July. Bitcoin Suisse, FalconX, STOKR and CoinFlip took licences across the same weeks, and Strike Europe secured full authorisation covering all 27 member states. Bybit and BitGo moved their European entities through the transition arrangements as national regimes expired.

A second track ran alongside it, and it is not one jurisdiction. Axi took a licence from the Financial Services Commission of Mauritius, Payward registered as a virtual asset service provider in the British Virgin Islands, Bullish won Gibraltar approval for tokenised securities trading, and Bitcoin Suisse received financial services permission in Abu Dhabi. Bitcoin Suisse now holds European authorisation and a Gulf permission granted fourteen days apart. Firms are buying optionality on jurisdiction, and paying for two regimes to keep it.

The Federal Reserve Board issued and terminated enforcement actions against bank holding companies on 18 June, 25 June, 2 July and 9 July, four consecutive Thursdays without a break. Six actions landed in four weeks, covering Manufacturers and Traders Trust, Bank of Eufaula, Small Business Bank, TS Banking Group and a terminated action with Jiko Group.

Crypto licences granted, 7 June to 11 July 2026. Bitcoin Suisse appears twice

Central banks turned their research toward the same subjects the market is funding. The Bank for International Settlements and the European Central Bank published papers on the macroeconomics of stablecoins on 23 June and on artificial intelligence and monetary policy on 6 July. The Federal Open Market Committee released the minutes of its 16 and 17 June meeting on 8 July, and the London Foreign Exchange Joint Standing Committee published three sets of minutes on 2 July.

Infrastructure build-out

Robinhood Chain launched its mainnet on 1 July with a complete institutional stack live the same day. BitGo provided custody, Maple provided onchain credit through syrupUSDG, Chainalysis provided automatic token monitoring, 0x provided swap liquidity and cross-chain access, and the network adopted Chainlink at launch. A regulated blockchain reached production readiness in one day.

Institutional custody drew ten firms in a week. Fireblocks and Figment enabled staking under qualified custody, BitGo added qualified custody for an SEC-registered yield-bearing security, and BNY expanded its relationship with Circle on institutional stablecoin services. Binance and Bybit both launched triparty banking arrangements, Kraken went live on Trever for European prime brokerage, and Anchorage Digital integrated with Binance's network.

Stablecoin settlement rails drew fourteen firms. Crossmint and Paga built multi-chain infrastructure for Africa, INFINIOS signed with Circle, and Kyriba partnered with Merge to bring stablecoin payments into corporate treasury management. In cross-border payments, Citi built round-the-clock dollar clearing with Siam Commercial Bank, Modern Treasury took a stablecoin-native mandate from Depa Finance, and Nuvion extended real-time transfers through Visa Direct. Not one participant in either segment disclosed a round size.

Firms active in each infrastructure segment

Banking modernisation

Credit unions became the sector's most contested customer. Clutch reported that six of the ten largest credit unions now run on its artificial intelligence platform, with a seventh going live in July. Glia, Alogent, Personetics, Scienaptic and Algebrik all moved on the same buyer. Jack Henry expanded its work with Google Cloud on security for banks and credit unions, and Stablecore, Circuit and Curql opened an early-access stablecoin programme for the sector.

Mortgage lending moved on income verification. Sallie Mae selected Nova Credit for income verification, Cloudvirga integrated Plaid into its Tropos platform, and Blend extended its MeridianLink integration. The document-based income check is being replaced by direct data access across the origination stack.

Corporate actions

Crypto treasury companies moved in opposite directions. Bitmine Immersion Technologies raised its Ether holdings from 5.54 million to 5.74 million tokens across the period, adding roughly 200,000 Ether. Eightco Holdings reported total holdings falling from $472 million on 18 June to $397 million on 9 July. Two balance sheets, one accumulating and one contracting, are the whole of this activity.

Grayscale filed officer compensation disclosures for eight crypto exchange-traded products on 2 July, covering its Bitcoin, Bitcoin Mini, Ethereum Classic, Chainlink, XRP, Dogecoin, Sui Staking and CoinDesk Crypto 5 vehicles. Eight sibling trusts moved on one parent decision.

Share repurchase authorisations came from Nakamoto, HashKey, Canton Strategic, BitGo, AMTD, Strategy, Nu Holdings and Yiren Digital. Nu Holdings authorised the largest at $1 billion over twelve months, BitGo authorised $50 million, and Strategy announced a digital credit capital framework alongside its own repurchase authorisations. No new authorisation appeared after 2 July.

Outlook

The Commodity Futures Trading Commission consultation is the regulatory event that matters into August. Perpetual futures on unlisted equity are already scaled, already concentrated in one venue, and already collateralised by tokenised stock. A rulemaking that begins after the market has formed sets the terms for every venue now holding the volume.

Jurisdiction has become a product decision. Firms are holding European authorisation and a second permission in the Gulf or an offshore territory at the same time, and the cost of running two regimes is now a budgeted line. Expect more dual-track licensing before the quarter closes.

Priced deals in stablecoin settlement are the thing to watch in capital markets. Firms have assembled across settlement rails and cross-border payments without a single disclosed round between them, and segments do not stay unpriced once institutions of Citi's and BNY's size have committed engineering to them.

The clearest line these numbers draw concerns who the plumbing is being built for. The largest cheque of the period financed the financial layer of a robotics company. Visa's payment partner for the agent economy is an artificial intelligence lab. Fintech is spending 61 cents of every disclosed dollar on infrastructure for money that moves without a person touching it, and the derivatives market it built on an unlisted company reached $7.1 billion at a single venue before its regulator opened a consultation.

Method and Source

Source: Cantica, The Bright Minded’s fin-tech intelligence layer. Deal, regulatory and corporate activity tracked from 7 June to 11 July 2026. Concentration analysis and the classification of capital by destination are The Bright Minded’s own calculations.

Editor's note

Every piece published on The Bright Minded goes through careful verification, but mistakes can happen. If you spot an error, have additional information, or want to flag anything, write to rosalia@thebrightminded.com.