The CFTC Just Approved the First Regulated Bitcoin Perps in US History. Here Is Why That Took So Long

The CFTC approved the first regulated bitcoin perpetual futures in the US on May 29, 2026. What perps are, why they thrived offshore for a decade, and what changes now.

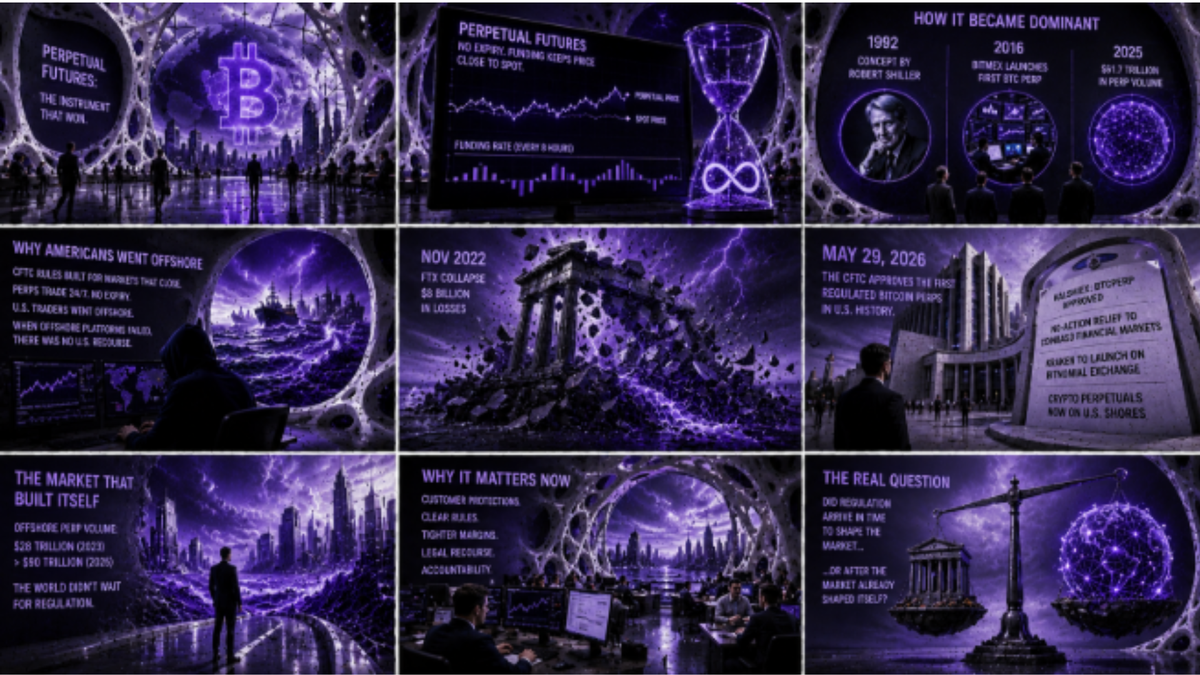

Perpetual futures are the dominant instrument in global crypto markets. They generated $61.7 trillion in trading volume in 2025 — more than three times global spot crypto trading volume the same year, per CryptoQuant data.

American traders have been participating in them for years. Until May 29, 2026, none of it happened on a regulated US exchange.

What a perpetual future is and how it became dominant

A standard futures contract expires on a fixed date. A trader who wants continuous exposure to bitcoin has to keep rolling from one dated contract into the next — closing the expiring position and opening a new one, each time absorbing the cost and friction of the switch.

A perpetual future is a futures-style contract with no expiration date at all. The trader holds the position as long as the trade makes sense. A funding rate mechanism — small periodic payments exchanged between long and short positions every eight hours — keeps the perpetual price anchored close to the spot price of the underlying asset.

The concept was first proposed by Nobel Prize-winning economist Robert Shiller in a working paper circulated through Yale's Cowles Foundation in 1992, originally designed to create derivative markets for illiquid assets like real estate and income indices.

Crypto adopted it first. BitMEX launched the first bitcoin perpetual swap in 2016, and the instrument spread rapidly across offshore exchanges throughout Asia and Europe. By 2025, perpetuals accounted for more than 70% of all trading volume on centralized crypto exchanges globally, per CryptoQuant.

The fintech and crypto infrastructure that grew around them — exchanges, clearinghouses, market makers — became one of the fastest-scaling segments of the global financial system, entirely outside US regulatory reach.

Why American traders went offshore

The Commodity Futures Trading Commission (CFTC) is the federal agency responsible for regulating US derivatives markets, and its statutory framework was built around markets that close overnight and on weekends, with fixed settlement dates and standard clearing structures.

Perpetuals trade around the clock, seven days a week, with no settlement date. The CFTC treated the instrument as something its existing rules could not accommodate, rather than something its rules needed to evolve to address.

The consequence was predictable. American traders who wanted access to perps went offshore — to Binance, Bybit, and until its collapse in November 2022, FTX. They used virtual private networks (VPNs), offshore accounts, and indirect routing methods that regulators were aware of but had not moved to resolve. When those offshore venues failed, US traders had no domestic legal recourse.

FTX's collapse cost its customers $8 billion in losses, per the sentencing finding of US District Judge Lewis Kaplan in March 2024. CFTC Commissioner Kristin N. Johnson identified the mechanism directly in an August 2024 statement: an absence of customer protection rules and gaps in regulation enabled the misappropriation of billions in customer funds deposited with FTX.

What happened on May 29

CFTC Chairman Michael S. Selig, sworn in as the Commission's 16th Chairman in December 2025, approved KalshiEX LLC's BTCPERP contract on May 29, 2026 — a perpetual futures product referencing the spot price of bitcoin, trading on Kalshi's CFTC-regulated designated contract market, per the agency's official approval order.

Simultaneously, the CFTC granted no-action relief to Coinbase Financial Markets, allowing it to route US clients into global perp and options liquidity — including Deribit, which carries tens of billions of dollars in bitcoin options open interest — through a CFTC-registered futures commission merchant structure.

Kalshi, in its May 29 launch announcement, described the BTCPERP as its most significant product expansion since the introduction of event contracts. Kraken announced the same day it would launch CFTC-regulated perpetuals within 30 days through Bitnomial Exchange — recently acquired by Kraken's parent company Payward — giving US traders access to perpetuals integrated alongside spot and margin trading on a single interface, per the Kraken blog.

The approvals apply only to cryptocurrency-linked perpetuals. Any contracts tied to other asset classes require separate regulatory evaluation, per the CFTC's accompanying policy statement.

The market that built itself without waiting

While the CFTC deliberated, offshore perp markets scaled into one of the largest financial instruments ever created. Offshore perpetuals grew from $28 trillion in annual volume in 2023 to over $90 trillion in 2025, per Kalshi's launch announcement.

Intercontinental Exchange (ICE), owner of the New York Stock Exchange, announced this week it is developing oil perpetual futures for trading in Europe and Asia in partnership with OKX — a direct signal that the instrument's utility has moved well beyond crypto into speculation on real-world assets.

The Standard Chartered decision to cut 7,800 back-office jobs while simultaneously absorbing a crypto custody business illustrates the same dynamic from the institutional side: traditional financial firms are no longer treating crypto derivatives as peripheral. They are building around them.

What changes now

Bringing perpetuals onshore under CFTC oversight changes who is accountable when something goes wrong and what protections traders carry inside the system.

The CFTC's own policy statement accompanying the May 29 approvals included explicit language warning that crypto derivatives remain highly speculative and that leverage can magnify losses rapidly. Offshore platforms have offered leverage up to 100 times notional value. The regulated US versions operate within tighter margin requirements.

The $61.7 trillion in 2025 perpetuals volume accumulated because perpetual futures solve a genuine problem — continuous price exposure without the drag of contract rollovers — and the demand for that solution existed long before a regulatory framework did.

What May 29 represents is the moment US regulation arrived at something that had been operating at scale for years, decided to participate, and started setting the terms. Whether that moment came early enough to shape the market, or late enough that the market had already shaped itself, is a question worth sitting with.

Editor's note

Every piece published on The Bright Minded goes through careful verification, but mistakes can happen. If you spot an error, have additional information, or want to flag anything, write to rosalia@thebrightminded.com.