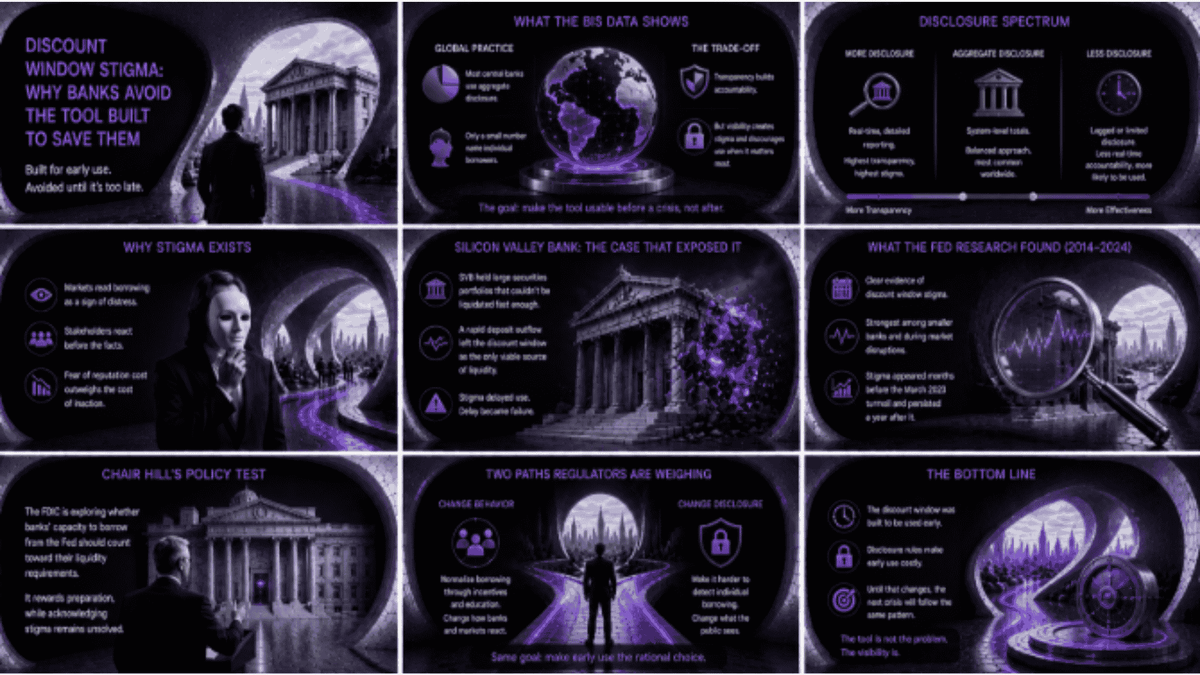

Discount Window Stigma: Why Banks Avoid the Tool Built to Save Them

The BIS June 2026 Quarterly Review confirms a five-decade problem: banks avoid central bank lending facilities because using them signals distress.

The Bright Recap

FDIC Chair Travis Hill said that the agency is exploring whether discount window borrowing capacity should count toward bank liquidity requirements. The BIS June 2026 Quarterly Review shows why this matters: banks avoid central bank lending facilities because being seen using them signals distress, a problem regulators have not solved in fifty years.

To know more about this topic, read our related articles:

- BIS June 2026 Review on settlement risk

- Wall Street's resistance to new infrastructure

- Financial technology explained

Bright Answers

What is discount window stigma?

It is the reluctance of banks to borrow from a central bank's lending facility because doing so, if discovered, is read by markets as a sign of financial distress.

Why don't banks use the discount window more often?

Central banks disclose borrowing data, even in aggregate form, and banks fear that being identified as a borrower will trigger deposit withdrawals or speculation about their stability.

Has any regulator solved the discount window stigma problem?

No. FDIC Chair Travis Hill said in June 2026 the stigma problem remains unsolved, even as the agency explores new incentives for banks to stay borrowing-ready.

Discount window stigma keeps banks from borrowing the moment a funding gap appears, even though that early borrowing is exactly what the facility is designed to encourage. The BIS June 2026 Quarterly Review confirmed this pattern across nearly every central bank surveyed: institutions favour aggregate disclosure over naming individual borrowers, because identifying a bank as a discount window user discourages the very use the facility exists to support.

FDIC Chair Travis Hill gave that finding a live US policy test this week, telling that the agency is exploring whether banks' capacity to borrow from the Federal Reserve should count toward their liquidity requirements, while acknowledging the stigma problem remains unsolved.

Lending facilities only work as intended if banks draw on them before a funding gap becomes a crisis. Disclosure regimes built for public accountability make that early use visible, and visibility is what markets read as distress.

What the BIS data shows about disclosure

Central banks face a direct trade-off between transparency and effectiveness when disclosing lending facility usage. Aggregate reporting is the dominant global practice, with only a small number of jurisdictions disclosing individual counterparty names. Disclosures that reveal or imply support to a specific institution can create stigma and discourage use during the episodes when use matters most.

The Federal Reserve reduced the granularity of its weekly discount window disclosures during the Covid-19 pandemic, consolidating reporting to the system level to protect borrower confidentiality. The Bank of England goes further, publishing its own discount window data with a five-quarter lag, accepting less real-time public accountability in exchange for a higher likelihood that banks will actually use the facility when they need it. The trade-off is not unique to central banking. Any regulated fintech sector built on disclosure faces the same choice between transparency and the behaviour transparency discourages.

Why Silicon Valley Bank changed the calculation

Hill pointed directly to the Silicon Valley Bank failure as the case that exposed how badly this trade-off can go wrong. Large banks holding hundreds of billions of dollars in securities cannot liquidate those holdings fast enough to cover a rapid deposit outflow, which leaves central bank borrowing as the only viable source of liquidity once an outflow accelerates past a certain speed. Research published by the Federal Reserve Bank of New York, revised in March 2026, found clear evidence of discount window stigma between 2014 and 2024, concentrated among smaller banks and around market disruptions, with stigma emerging months before the March 2023 banking turmoil and persisting a year after it.

The two paths regulators are weighing

Hill described two directions under consideration. Building enough routine comfort with borrowing that drawing on the window stops reading as a warning sign would ask banks and markets to change their behaviour around the existing disclosure standard, while making it structurally harder for outsiders to detect when a bank has borrowed at all would ask regulators to change the disclosure standard itself. Hill's own proposal, treating borrowing capacity as a counted liquidity asset, sits closer to the first option: it rewards preparation to borrow rather than concealing the act of borrowing.

The same institutional reluctance shows up outside banking. Wall Street's resistance to adopting new settlement infrastructure has never been about whether the technology works. It has been about who carries the visibility cost of changing first.

What this means for the next stress event

The BIS review's broader point is that this is not a uniquely American problem. Every central bank surveyed balances the same trade-off between accountability and effectiveness, and most have settled on some version of aggregate disclosure as the least damaging compromise available. The New York Fed's research found that stigma cannot be explained by a lack of operational readiness alone, and that it is associated with higher failure risk among the banks most affected by it.

Hill's proposal acknowledges that the discount window's design and its disclosure regime work against each other: a facility meant to be used early and often sits inside reporting rules that punish early and frequent use. Fifty years after the tool was built, regulators are still trying to make using it look as routine as it was designed to be.

Editor's note

Every piece published on The Bright Minded goes through careful verification, but mistakes can happen. If you spot an error, have additional information, or want to flag anything, write to rosalia@thebrightminded.com.