Can You Put Crypto in Your 401(k) in 2026? The Retirement Data Behind the Access Debate

Can you put crypto in your 401(k) now? The Federal Reserve's 2025 data on retirement savings changes what the access debate actually means.

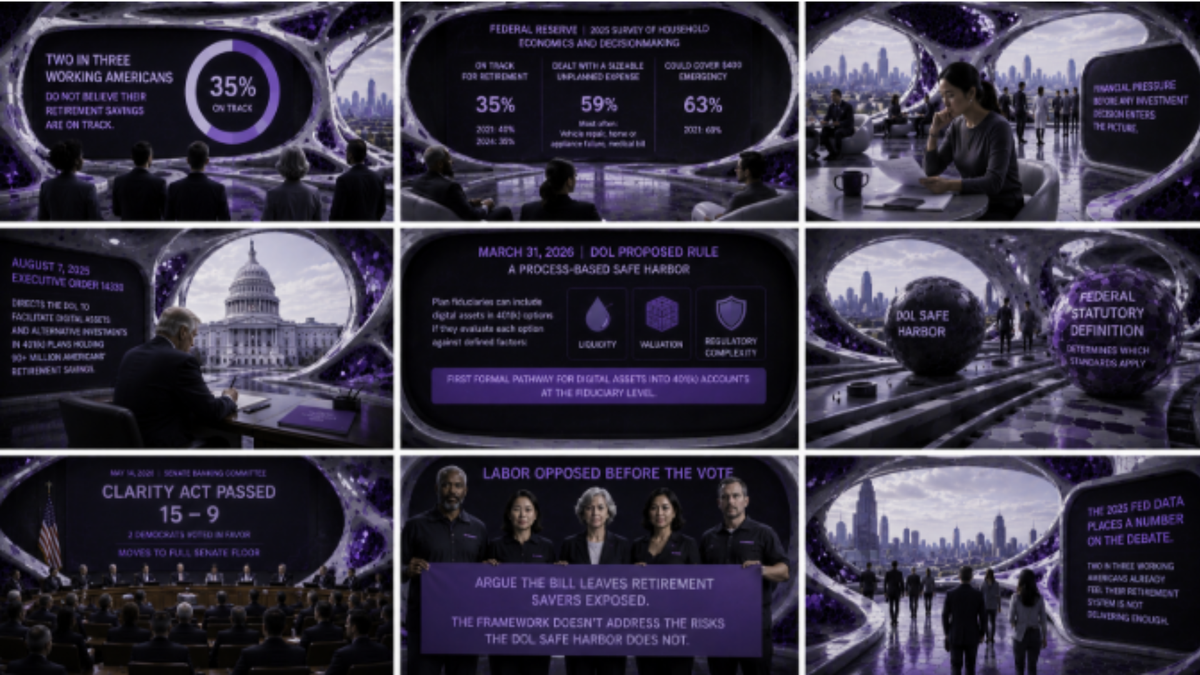

Two in three working Americans do not believe their retirement savings are on track. The Federal Reserve published that figure on May 13, in its 2025 Survey of Household Economics and Decisionmaking. The share who feel on track stands at 35 percent, down from 40 percent in 2021. That is the population Washington is now formally inviting to add crypto to their 401(k) accounts.

What the retirement numbers show

The Federal Reserve has fielded its annual household survey each autumn since 2013, tracking financial well-being, savings, credit, housing, and employment across U.S. adults. The 2025 edition shows overall stability, with meaningful declines concentrated among younger adults, low-income households, and Black adults. For the broader working population, the retirement figure sits at 35 percent on track, unchanged from 2024 and five percentage points below where it stood in 2021.

Among adults surveyed, 59 percent dealt with at least one sizeable unplanned expense over the prior year, most often a vehicle repair, a home or appliance failure, or a medical bill. The share who could cover a hypothetical $400 emergency using cash or its equivalent stood at 63 percent, down from 68 percent in 2021. For the two in three who do not feel their retirement savings are on track, the financial pressure is both chronic and familiar before any investment decision enters the picture.

How the 401(k) crypto pathway opened

Executive Order 14330, signed by President Trump on August 7, 2025, directed the Department of Labor to facilitate digital assets and alternative investments in the 401(k) plans holding more than 90 million Americans' retirement savings. The DOL published its proposed rule on March 31, 2026, creating a process-based safe harbor: plan fiduciaries can include digital assets among the investment options they offer employees, provided they evaluate each option against defined factors including liquidity, valuation, and regulatory complexity.

The rule is the first formal mechanism by which plan managers can bring digital assets inside employer-sponsored retirement accounts at the fiduciary level, and the safe harbor it creates defines how they are required to evaluate those assets before doing so. The federal statutory definition of those assets, which determines which regulatory standards apply to each one, belongs to legislation whose Senate committee vote concluded on May 14.

The framework still being written

The CLARITY Act, the central piece of US fintech legislation currently before Congress, would establish that statutory classification, determining which standards apply to each digital asset and what a completed prudence review looks like in practice. The Senate Banking Committee passed it 15-9 on May 14, with two Democrats voting in favor, sending it to the full Senate floor.

Five of the country's largest labor unions had filed formal opposition before the vote, arguing that the bill's framework would leave retirement savers exposed in ways the DOL safe harbor does not address. The structural gap they identified between the two policies is covered in The Bright Minded's earlier coverage of the union opposition filed before Thursday's vote.

The Federal Reserve's 2025 data places a number on the population at the center of that debate: working Americans who, by a ratio of roughly two to one, already feel the retirement system they have is not delivering enough.

Editor's note

Every piece published on The Bright Minded goes through careful verification, but mistakes can happen. If you spot an error, have additional information, or want to flag anything, write to rosalia@thebrightminded.com.